Miami Real Estate

Miami’s real estate market is evolving, and Cove Miami is set to redefine luxury waterfront living. This exclusive high-rise development offers unparalleled elegance, breathtaking ocean views, and world-class amenities in one of the city’s most desirable locations. A...

Real Estate

The Florida real estate market in 2024 experienced fluctuations driven by economic conditions, interest rates, migration trends, and climate-related challenges. With a mix of opportunities and risks, buyers, sellers, and investors had to navigate a dynamic...

Miami Real Estate

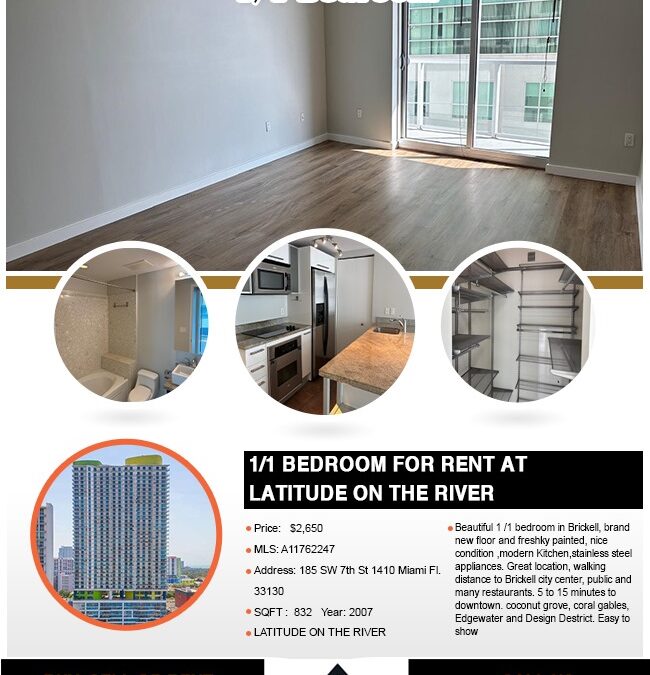

Here’s a clean and well-structured rewrite for your website listing: Beautiful 1-Bedroom Condo in Brickell – $2,650/Month 📍 185 SW 7th St #1410, Miami, FL 33130 📌 MLS#: A11762247 | Status: Active | Available: 03/12/2025 Property Details: Rent: $2,650/month Bedrooms: 1...

Miami Real Estate

Hedge fund giant Citadel, led by billionaire Ken Griffin, is set to transform Miami’s skyline with its new 54-story headquarters at 1201 Brickell Bay Drive. Foster + Partners designed this iconic glass tower, which will redefine Miami’s financial district. Key...

Miami Real Estate

Welcome to the latest Latitude on the River market update for February 2025! Whether you’re looking to buy, sell, or rent a condo in Miami, this report provides the most recent pricing trends and market activity to help you make an informed decision. Latitude on...

Real Estate

Introduction The Florida real estate market in 2025 continues to be a dynamic and attractive investment opportunity, particularly in Miami. With the latest economic policies under President Donald Trump’s administration, including trade tariffs, immigration reforms,...

Real Estate

As of February 2025, Florida’s real estate market exhibits a mix of stabilization and growth, with regional variations influenced by factors such as inventory levels, buyer demand, and infrastructure developments. Statewide Trends: Home Prices: The median home...